Rare earth elements (REEs) hit mainstream media in recent months, again. Critical minerals dependencies on China, which were clearly visible and avoidable for the past decade, have come back to roost as Western countries neglected technical development in favor of low-cost imports and are now scrambling to hedge against supply risks as China continues to leverage its control in geopolitical negotiations. Combined with the booming AI sector and data centers, converging commentary on REEs and data centers is fueling fear around the growth prospects plagued by materials shortages.

To explore if critical minerals shortages really threaten the growth of data centers, Lux applied its Raw Materials Criticality Framework to assess raw materials through two dimensions — supply risk and criticality — to quantitatively identify shortfalls and opportunities.

Methodology for assessing critical minerals in data centers

For this analysis, Lux assumed an aggressive scenario in which installed data center capacity doubles to 240 GW by 2030 — implying 120 GW of new build in the coming years. Drawing on company presentations and third-party reports, a 100-MW reference data center was used to estimate the critical minerals required, isolating the IT hardware components as outlined by the U.S. Geological Survey. The analysis focuses on critical minerals of strategic importance and is not intended to be a thorough assessment of all materials or structural and electrical infrastructure.

Key findings from Lux’s critical minerals analysis

Data center growth is poised for raw materials stability in the next five years, and likely beyond. Even under the aggressive doubling scenario, global production will sufficiently meet demand for raw materials. Nearly all materials required for data centers represent 10% or less of annual global production. Although demand will rise, the volumes required are relatively small compared to other technologies. For instance, producing 1 GW of data center capacity requires approximately 30 tonne of silicon, based on silicon intensity benchmarks — far less than the 5,500 tonne needed for 1 GW of solar capacity. This scale discrepancy highlights the distinct differences around long-term raw materials challenges. As demand for green hydrogen, renewables, and EVs grows, data centers are still likely to outcompete these technologies for supply access.

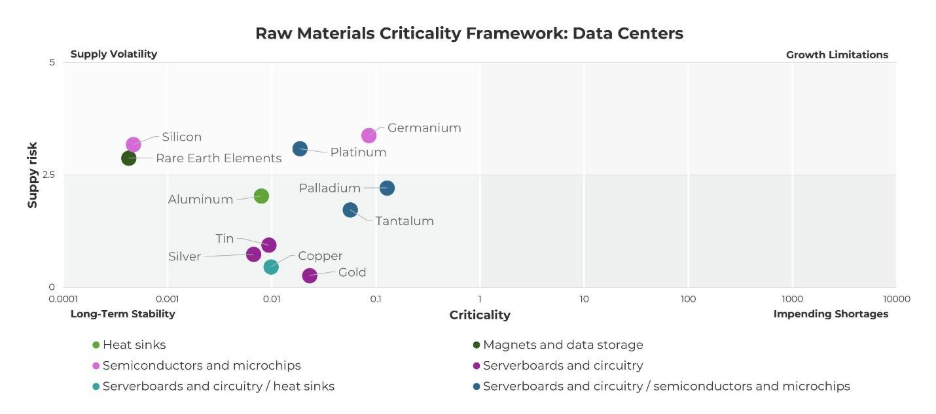

Supply risk for REEs and other critical minerals is high but not exclusive to data centers. Global supply for silicon and germanium for semiconductors and microchips (pink bubbles) and REEs for magnets and data storage (dark green bubbles) remain heavily controlled by China, while platinum for server boards and circuitry and semiconductors and microchips is concentrated in South Africa. Particularly for REEs, which continue to be used as instruments of geopolitical negotiations, hedging against supply risk will be critical for long-term stability. Building a parallel supply chain to replace China’s REE capacity is highly unlikely, but innovations tapping into novel sources such as volcanic tuffs, mine tailings, and deep-sea mining are currently being explored and could be sufficient for the low volumes required in data centers.

Innovation opportunities for data centers will fall primarily outside of core IT hardware. While silicon and germanium exhibit high supply risk, the value chain is highly insulated in terms of both raw materials supply and disruptions from external innovations. Leading foundries, such as Taiwan Semiconductor Manufacturing Company, Samsung, and Intel, remain committed to silicon-based architecture in their product roadmaps, indicating the industry’s confidence in the near to midterm supply of these raw materials. Their tight control over the evolution of the space limits opportunities to substitute or materially innovate around these critical minerals. Instead innovations in liquid-cooling and novel thermal management materials present viable entry points for companies looking to capitalize on data center buildouts.

Outlook: Why critical minerals won’t slow data center deployment

Shortages of critical minerals will not hinder new data center deployments. Although demand will increase, the relatively modest materials requirements and resilient supply chains position data centers well in terms of supply stability and criticality. While critical minerals remain important, data centers do not face the same constraints as renewables, EVs, or hydrogen technologies.

Instead, delays and cancellations will more likely stem from community opposition and interconnection bottlenecks — the latter often extending project timelines by several years in the U.S. and Europe. While major tech companies remain financially committed to expanding data center capacity, the timeline for growth remains uncertain. Strong expansion is inevitable, but the most aggressive 2030 projections appear unlikely. A more moderate, extended buildout is expected, which will give the supply chain time to address materials needs and coordinate bulk infrastructure development to support server deployment.

To learn more about these findings, connect with a Lux analyst.