In response to depleting fish stocks and increasing global aquaculture production, research and development around single-cell proteins (SCPs) is making headway as an alternative ingredient to replace fish meal in aqua and other livestock feeds. However, this renewed interest is also paving the way for SCPs in food applications. As SCPs become more relevant to feed and food producers alike, it will be important to distinguish between developers on their technical capabilities and market approaches.

Lux recently reported on the strategic impact of synbio and identified four key elements to navigate differentiation within synthetic biology applications. Those key elements are feedstock, microorganism, production infrastructure, product and market. Using this framework, this insight examines several SCP developers targeting the feed and food industries and leverages that information to outline additional concerns clients should consider for each key element.

Key Elements for synbio success

Feedstock: Do you have access to an inexpensive feedstock?

- Microbes metabolize simple organic compounds like sugars, alcohols, organic acids, and hydrocarbons. Production often requires proximity to a gas feedstock source (i.e., ethanol plants, flue gas, and biogas derived from agricultural waste) to minimize unnecessary production costs. Using methane or CO2 as a feedstock offers producers of those gases a way of reducing their total greenhouse gas. Other potential substrates for SCP include first- and second-generation sugars, starch, cellulose, or woody biomass. However, the woody biomass must be pre-treated to separate it into lignin, hemicellulose, and cellulose components before converting hemicellulose to xylose and cellulose to glucose.

Microorganism: How does your microorganism perform compared to competitors?

- SCP is derived from bacteria, yeast, or other fungi. Bacteria are usually higher in protein (50 to 80%) than yeast (40 to 60%) or fungi and have more rapid growth rates.

- Competitors are exploring the use of directed evolution and genetic modification to optimize commercially relevant traits or functional attributes, including biomass conversion rate, product consistency, and nutritional composition. Genetic modification for ingredients that include whole cells or whole-cell lysates faces regulatory scrutiny.

Production infrastructure: Not only does capacity matter, but ownership strategy matters as well (build/own/operate vs. toll manufacturing)

- Few SCP producers have reached large-scale production due in part to high investment costs (typical facility construction costs are in the hundreds of millions of dollars) and challenges with product validation in target markets. Lux recently spoke with White Dog Labs’ CEO, Bryan Tracy, who commented that developers must be able to produce enough protein at pilot scale to support extensive testing and feeding trials, all prior to first product sales. Based on Lux’s discussions with SCP innovators, an appropriate goal for scaled production is 10,000 metric tons per year (MT/yr).

Product and market: What are you selling and for how much?

- The main strategy seen by SCP producers is to target feed, specifically as a sustainable alternative to fish meal. Successful feeding trials and testing are driving regulatory approval.

- The application of SCP as a food ingredient will need to overcome public perception challenges and navigate uncertain regulatory hurdles (i.e., novel food authorization). SCP producers will need to not only deliver on taste, palatability, cost, and quality but also demonstrate competitive advantages (i.e., sustainability and nutritional profile) over other alternative proteins currently on the human food market. The progression of cellular agriculture and other fermented foods may support the transition of the public mindset toward widespread acceptance of SCP for food.

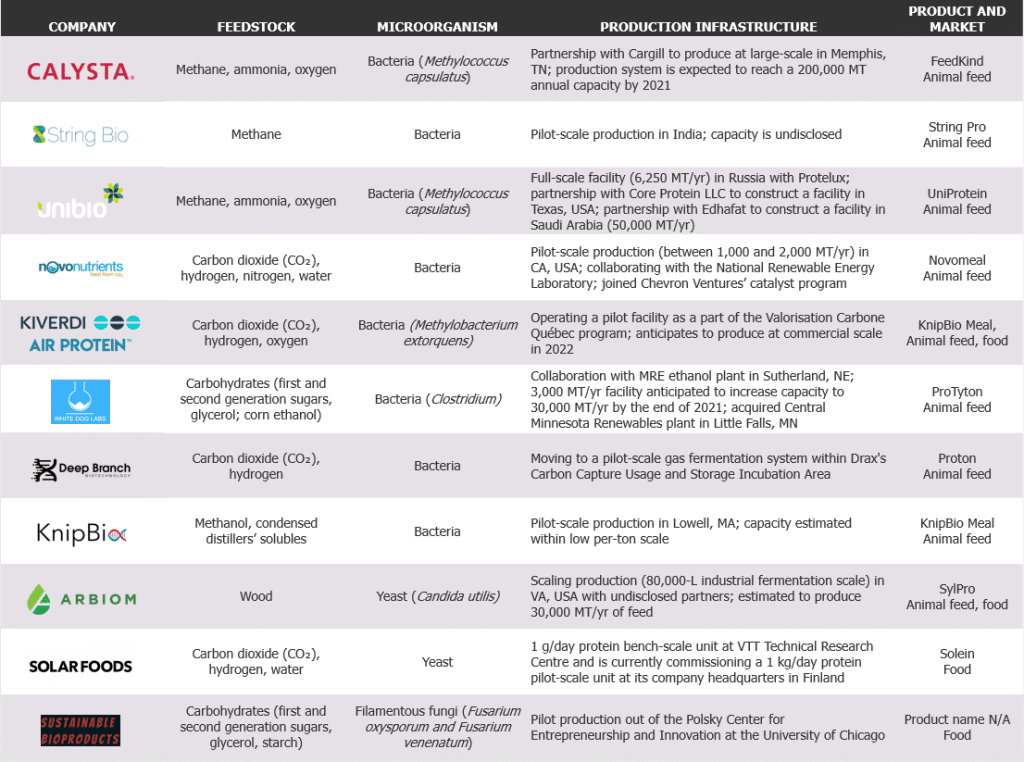

Differentiating competitors by key elements

In the figure below, we differentiate several SCP developers targeting the food and feed industries across four key elements: feedstock, microorganism, production infrastructure, product, and market. Based on this comparison, we summarize the takeaway for each key element and discuss additional concerns below.

Fig. 1. Comparison of the key elements seen by single-cell protein developers targeting feed and food

Feedstock availability will be paramount

Low-cost feedstocks for SCP production are typically byproducts of industrial processes. For instance, KnipBio claims to have developed its system to use condensed distillers’ solubles, a byproduct of ethanol fermentation, to achieve cost-competitiveness with fish meal. Other competitors are using raw emissions from cement manufacturing facilities or oil refineries. To that end, strategic partnerships within industries producing compatible byproducts, such as the energy industry, are key. Recent support seen from federal governments and oil and gas players (BP Ventures) suggests that SCP developers will find stability in sourcing their feedstocks.

Systems using CO2 as feedstock also require hydrogen gas as a microbial energy source. Hydrogen sources include water electrolysis, which is the most expensive component due to today’s high electricity prices (see the Water Electrolysis Tech Page), or a byproduct of concrete production. Solar Foods plans to source hydrogen generated from electrolysis of water powered by solar energy; however, the system’s high energy consumption may pose significant challenges at a large scale.

Advanced strain development leads to commercial optimization

SCP developers are selecting and optimizing microbial strains based on growth rate and protein content. As it stands now, the specific strain is less relevant than a developer’s efforts to optimize the traits of strains. This is most evident in those that target human food applications, which have not settled on an accepted microbial production platform. This may be due to the familiarity of traditional fermentation using yeast or consumer misconception that consuming bacteria is dangerous.

SCP food and feed products are not currently produced from transgenic organisms, but developers are exploring future opportunities to improve key traits like nutrient conversion through these methods (e.g., String Bio, NovoNutrients, Kiverdi).

Production infrastructure differentiates the competition

Calysta and Unibio are leaders in large-scale production (both over 10,000 MT/yr) and have secured partnerships that will drive growth. Both companies’ production platforms are easily scalable through loop reactor technology that continuously delivers high utilization of gaseous feedstocks. They also claim lower energy usage and costs compared to traditional stirred tanks.

While companies using CO2 as a feedstock are identifying strategic partners, these technologies remain to be proven at the commercial stage. The high investment costs coupled with the reliance on hydrogen gas as an energy source may warrant a deeper technical and economic assessment. That said, strong competitors are identifying access to gas inputs and capital. This includes NovoNutrients, which recently joined Chevron Technology Ventures’ Catalyst Program.

Developers White Dog Labs and Arbiom, both using cellulose-derived feedstock, are currently moving to commercial-scale production. Both companies have conducted extensive testing of their protein ingredients with promising results in nutrition and sustainability.

Targeting the human food market will be a more challenging path to commercialization

SCP continues to generate interest for applications in aquaculture feed as companies validate their products with the industry (e.g., Calysta and Thai Union Group).

Solar Foods, Sustainable Bioproducts, and Kiverdi’s Air Protein are focusing solely on producing protein ingredients for human food applications; however, challenges facing commercialization in this intended market abound. These developers remain early-stage and have not achieved scaled production or regulatory approval. Solar Foods may have a marginal lead on others via its collaboration with players in the food industry to determine SCP performance in different food applications.

Conclusion

As SCP in food applications faces greater challenges in regulations and public perception than feed, expect developers to validate their products and overcome barriers to commercialization at different rates. However, successful developers targeting either industry will be those that gain access to potential waste stream partners and scale up. Likewise, companies with feedstock supplies, applicable waste streams, or fermentation capacity should look to exploit SCP. The time to engage with SCP is now, as future protein demand will insist on it.