What is Biogenic CO2?

Biogenic CO2 refers to the thermal or natural release of CO2 stored in biomass and other organic matter. CO2 can be generated through biomass combustion during power and heat production, fermentation, or other refinery processes. CO2 concentration in biogenic sources can vary widely, from as low as 6% to over 90%, leading to the use of a variety of carbon capture technologies. Biogenic CO2 is a nonfossil source of CO2, and therefore has a strong role to play in sustaining future low-carbon supply chains.

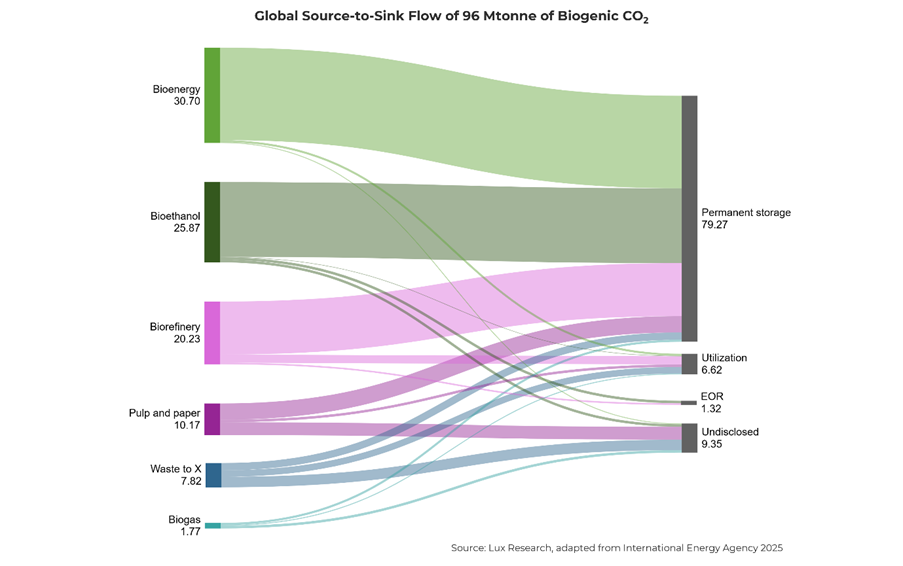

Which Projects Release Biogenic CO2 and What are Their Uses?

Bioenergy

In bioenergy, CO2 is emitted when biomass undergoes combustion to generate power. These flue gas streams have varying CO2 concentrations depending on the feedstock, but generally range between 6% and 14%. Of all sources of biogenic CO2, bioenergy has the largest average project capacity, 2 Mtonne/y CO2. Bioenergy with carbon capture and storage (BECCS) is an avenue to produce carbon credits. Hence, a significant amount of CO2 from bioenergy is directed toward permanent storage.

Bioethanol

CO2 is released as a byproduct of the fermentation of corn and sugarcane feedstocks in bioethanol production. This process generates CO2 with very high concentrations and in most cases does not require additional separation or processing. The lack of postprocessing dramatically reduces CO2 costs, which can be as low as USD 15/tonne. The U.S. leads in planned projects in this category due to the combination of abundant feedstock and high incentives; of the 32 projects, 28 are located in the U.S. The average project size is 0.81 Mtonne/y, showing a large volume of distributed small producers.

Biorefinery

In biorefineries, the CO2 emission source and concentration depends on the specific refining process used, such as fermentation, gasification, or pyrolysis. While biorefineries can produce a range of products, their main planned product with CCUS is ethanol, probably due to the stable nature of the ethanol industry and low cost of captured CO2. Facilities producing other products, such as renewable diesel, have struggled with the economics of launching CCUS projects. Some, such as Federated Co-operative Limited’s renewable diesel facility, have paused operations due to regulatory and economic uncertainty. Activity here is heavily concentrated in the U.S., with 75% of the planned biorefinery CO2 projected to be sourced from U.S. facilities, scheduled to launch by 2028. These are small facilities, and project capacities average 0.36 Mtonne/y.

Pulp and paper

In pulp and paper, the primary CO2 stream comes from the combustion of waste biomass to generate heat and power. These are large facilities requiring significant energy, and project capacities average 1.27 Mtonne/y. The project development timeline is similar to bioenergy’s, with multiple large projects planned for 2030 or later. These deployments are in regions with significant timber production, such as Norway, the U.S., and Japan.

Waste to X

Waste to X encompasses both waste-to-energy projects as well as some waste-to-e-fuels projects. In waste to energy, CO2 is sourced from the combustion of biomass waste products; in waste to fuels, it is generated as a process emission. There is a split in the handling of CO2 based on the source. Most of the e-fuels projects intend to use the CO2 within the process for their fuel production, while most waste-to-energy plants either plan to permanently sequester or have not disclosed their CO2 use. The projects are small, averaging 0.489 Mtonne/y, with no projects over 1 Mtonne/y. Regionally, the U.S. is absent here, and activity is entirely concentrated in Europe.

Biogas

Biogas upgrading, or the process of separating CO2 from methane, is a mature industry for carbon capture, often irrespective of decarbonization goals. Biogas, generated from the decay of organic matter has a high percentage of CO2, 30% to 50% by volume, and must be upgraded by filtering out CO2 using pre-combustion carbon capture technologies. Currently, a majority of this CO2 is vented, and the International Energy Agency is tracking just six total carbon capture utilization and storage (CCUS) projects in biogas. These projects are primarily in Europe (U.K., Denmark).

Challenges and Opportunities in Utilizing Biogenic CO2

Small-Scale Biogenic CO2 Projects Face Logistical Barriers to Carbon Capture and Storage

Biogenic sources, outside of bioenergy and pulp and paper, are characterized by small project capacities, presenting a logistical challenge for companies looking to provide storage services to these industries. Small projects (0–0.5 Mtonne/y) are the most common capacity size for all biogenic CO2 sources except pulp and paper. These projects largely rely on CO2 sequestration as the end-use, which also include on-site wells. For this, they need to partner with oil and gas companies or sequestration infrastructure developers like Summit Carbon Pipeline and Carbon America. Connecting smaller distributed CO2 sources with larger transportation networks can pose several logistical barriers, including crossing multiple state or country borders and securing hundreds of miles of property rights. Small-capacity projects with near-term timelines will need to address this challenge immediately, while larger-scale projects from bioenergy can benefit from networks being developed for cement or for other forms of power generation. Smaller-scale projects should aim to provide CO2 directly to fuel production facilities, or directly provide biogas for biomethanol production. Carbon capture from biogas will increase in the next five to 10 years. Currently, the challenges of centralizing biogas production keep producers from larger CCUS projects at bay, but the growing demand and monetization opportunities that come with biogenic CO2 will drive developers upgrading biogas to capture CO2 more diligently.

U.S. Leads Biogenic CO2 Supply but Faces Sequestration Bottlenecks and Policy Risks

The U.S. is the key producer of biogenic CO2 in the near term, owing to its high momentum within the bioethanol industry. But concerns over the safety and efficacy of CO2 sequestration may lead to sequestration project delays and cancellations, stranding an easy-to-access CO2 source. These projects are at risk from both an administrative and societal backlash. As the U.S. rolls back federal funding for decarbonization, landowners are increasingly fighting the Summit Pipeline in public forums, especially after recent news of CO2 leaks. These leaks were due to well corrosion, and the Environmental Protection Agency has yet to unveil new guidelines on well construction based on this leak. Additionally, permitting is a severe bottleneck in U.S. sequestration projects, with over 150 projects awaiting approval. In Europe, frameworks for cross-border CO2 transportation will be necessary to maximize the value of biogenic CO2. Clients can look at delays in sequestration as an opportunity to reallocate biogenic CO2 to utilization.

Sequestration of Biogenic CO2 May Undermine Decarbonization in Aviation and Chemical Sectors

Sequestration deprives the aviation and chemical sector from a key feedstock. Biogenic CO2 is a highly valuable commodity to the chemicals and sustainable aviation fuel (SAF) sectors as it provides a renewable alternative to fossil carbon; as such, it was expected that most biogenic CO2 would go to these industries. However, the analysis shows that most biogenic CO2 will still end up in permanent storage to generate carbon credits; such biogenic CO2 could have instead supported 200 e-SAF facilities or 500 e-methanol facilities, for example. This presents an interesting conundrum. At a system level, it does not matter where that biogenic CO2 goes to, as long as it leads to a net reduction in CO2 emissions. But what if sequestrating that biogenic CO2 means the chemicals and aviation sectors never get to fully decarbonize? Will countries ban the sequestration of biogenic CO2? Unlikely. This means chemicals and SAF companies will have to compete against everyone else looking to buy carbon credits. This is hard to do when companies are already paying up to USD 350/carbon credit from bioenergy, according to our sources.

The Lux Take

Biogenic CO2 is a highly valuable commodity and will continue to grow in value through the next 10 years. Although it’s an essential feedstock for chemicals and e-fuels, biogenic CO2 will have a growing role in CO2-removal markets, where it competes with carbon-credit-generating technologies. Smaller sizes for biogenic CO2-capture projects present logistical barriers in consolidating, but industry stakeholders with access to this grade of CO2 should explore ways to recirculate it back into existing supply chains.

For more insights on biogenic CO2, connect with us today.