In 2025, the EU implemented its Sustainable Aviation Fuel (SAF) mandate, requiring all departing flights (including those by non-EU airlines) to use a minimum of 2% SAF. This share will increase to 6% by 2030, 34% by 2040, and 70% by 2050. The mandate also includes a subtarget for e-SAF, derived from CO2 and hydrogen, starting at 1.2% of the fuel mix in 2030 and rising to 35% by 2050.

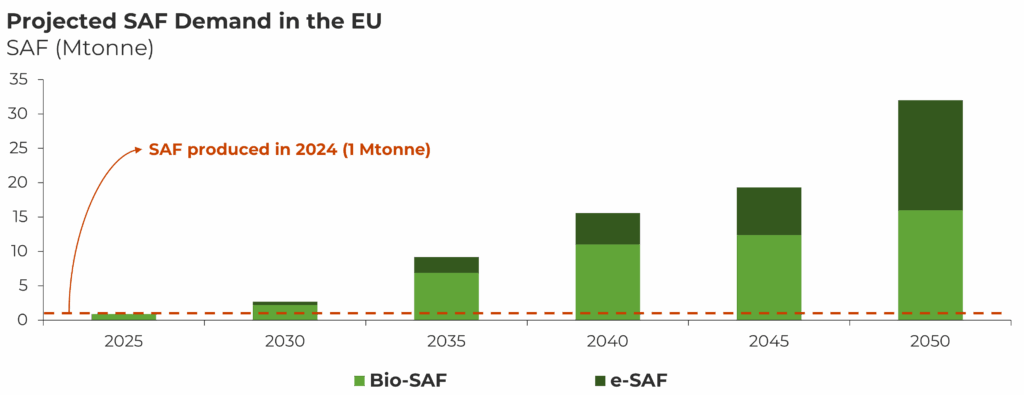

The EU consumes approximately 46 Mtonne of jet fuel annually. The 2% SAF mandate in 2025 creates an immediate demand for up to 1 Mtonne of SAF, rising to 2.7 Mtonne by 2030, 9.2 Mtonne by 2035, and 32 Mtonne by 2050. IATA estimates that only 1 Mtonne of SAF was produced globally in 2024. Before 2025, airlines adopted SAF voluntarily to meet internal net-zero targets. Starting in 2025, however, all airlines operating in the EU are required to use SAF under the new mandate.

Despite its ambitious goals, the EU’s SAF mandate will fall short for two key reasons:

- SAF supply will not meet mandated demand.

- Emerging SAF technologies remain prohibitively expensive, and enforcing their adoption could severely impact the EU’s aviation industry after 2030.

Understanding these challenges requires a closer look at the current SAF technology landscape.

Beyond the era of HEFA

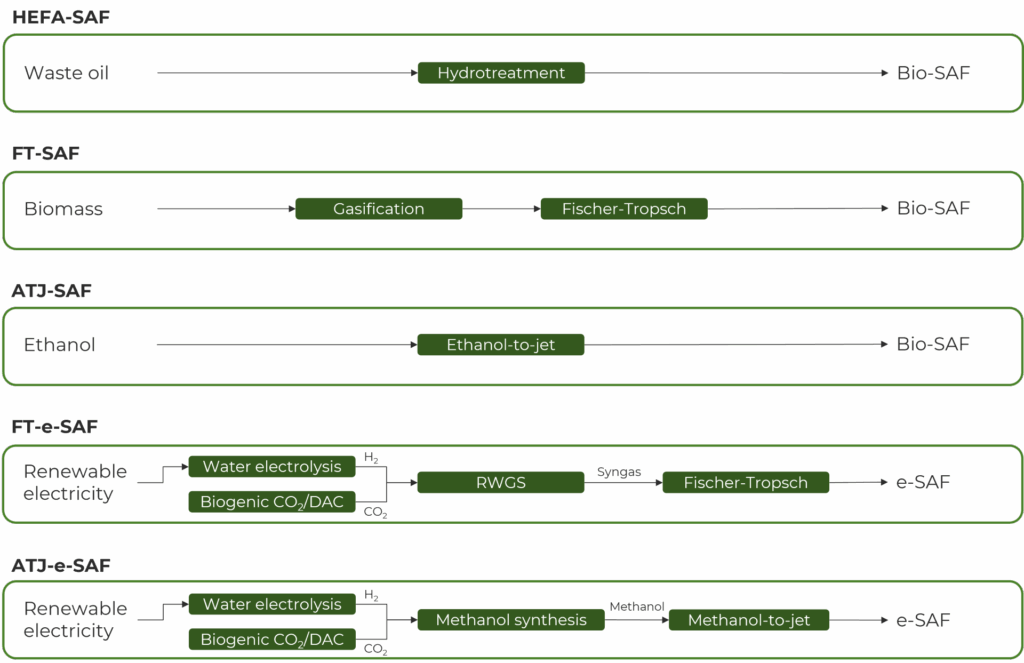

SAF is jet fuel produced from low-carbon feedstocks such as waste oils, biomass, ethanol, methanol, or CO2 combined with low-carbon hydrogen. Each feedstock requires a distinct conversion technology. Currently, hydroprocessed esters and fatty acids (HEFA), which converts waste oils into jet fuel, is the only commercially viable pathway. In 2024, all 1 Mtonne of SAF produced globally came from HEFA. Other technologies, including Fischer-Tropsch (FT; using biomass or CO2 and hydrogen) and alcohol to jet (ATJ; using ethanol or methanol), remain in development and are not yet commercial.

Despite being commercially scalable, HEFA technology alone cannot meet SAF demand. The EU prohibits the use of vegetable oil feedstocks from food or feed crops, due to environmental sustainability concerns, allowing only the use of waste oils like used cooking oil. However, according to a recent report from the IATA and Worley, there is not enough waste oil in the world to sustain the global demand for SAF if all of it were to be produced through the HEFA pathway. To meet the demand for SAF, production will need to scale through alternative technologies such as FT or ATJ.

The Cost of SAF

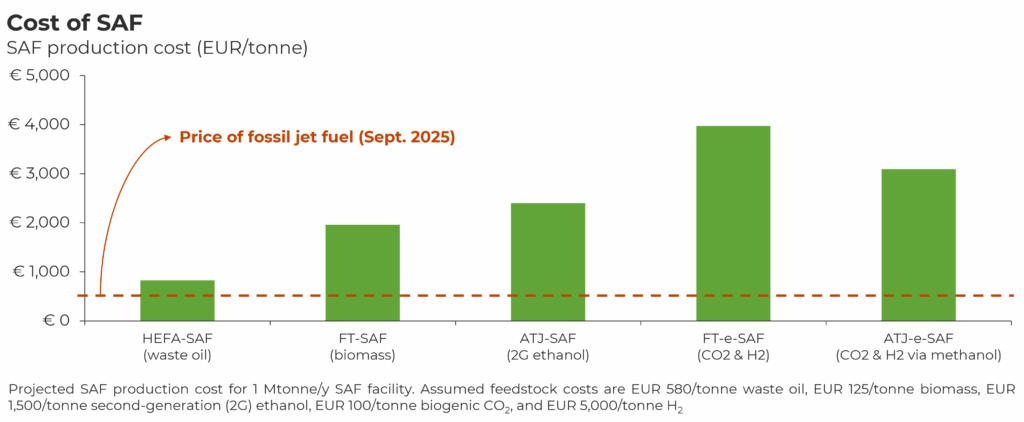

The key question in the SAF industry is cost. The EU Aviation Safety Agency (EASA)’s “2024 Aviation Fuels Reference Prices” report provides benchmark figures: HEFA-derived SAF costs EUR 1,460/tonne — more than double the average market price of fossil jet fuel at EUR 700/tonne.

However, the EASA’s pricing reflects 2024 conditions, while the mandate extends through 2050. A common counterpoint to EASA’s data is that emerging SAF technologies will lower costs over time. Indeed, more than 60 corporations and startups are developing novel SAF pathways that aim to tap into new feedstocks and, crucially, reduce production costs.

At Lux Research, we conducted a technoeconomic analysis of both current and emerging SAF technologies. For each SAF technology (HEFA, FT, and ATJ), we modeled production costs across various feedstock-technology combinations. The results reflect nth-type plants, assuming full scale-up and optimization, and represent the lowest expected cost for each technology, excluding major technological breakthroughs.

As seen from the results, SAF from any technology will remain more expensive than fossil jet fuel. HEFA-SAF is the cheapest option, but its use will plateau beyond 2030 due to a lack of waste oil feedstock. The next cheapest option is FT-SAF using biomass feedstock. This is a valuable technology pathway due to the much higher availability of biomass feedstock compared to waste oil; however, scaling biomass gasification technology required for FT-SAF is no easy feat as Fulcrum Bioenergy’s abandoned plant illustrates. ATJ-SAF could have been an affordable option, but since the EU bans the use of ethanol from food crops (for example, corn or sugarcane), the only eligible feedstock is 2G ethanol. 2G ethanol is not yet available at scale; aside from limited success by Raízen in Brazil, the space is literred with commercial failures as outlined in this excellent article by C&EN. This leaves us with e-SAF, which is a major pitfall of the EU’s SAF mandate.

e-SAF is produced from CO2 and H2, but the EU imposed strict feedstock requirements. Only biogenic CO2 or CO2 from DAC is permitted, while industrial CO2 is eligible only for a limited time and H2 must be derived from renewable electricity. Currently, two main pathways exist: FT and methanol to jet. With FT, CO2 and H2 convert into syngas, which then feeds an FT reactor to produce SAF. In methanol to jet, CO2 and H2 first convert into methanol, which is then refined into SAF. In both cases, e-SAF will be approximately 3–4× more expensive than fossil jet fuel, and this is even after assuming a generous green hydrogen price of EUR 5.00/kg. With our current portfolio of emerging technologies, SAF will remain highly expensive.

Who will pay for SAF?

The burden of complying with the EU’s SAF mandate falls on the jet fuel producers. The problem is that they will simply pass the compliance cost down to the airlines, which will have no choice but to pass it down to its customers: The result is that Europeans will pay a much higher price to fly compared to the rest of the world.

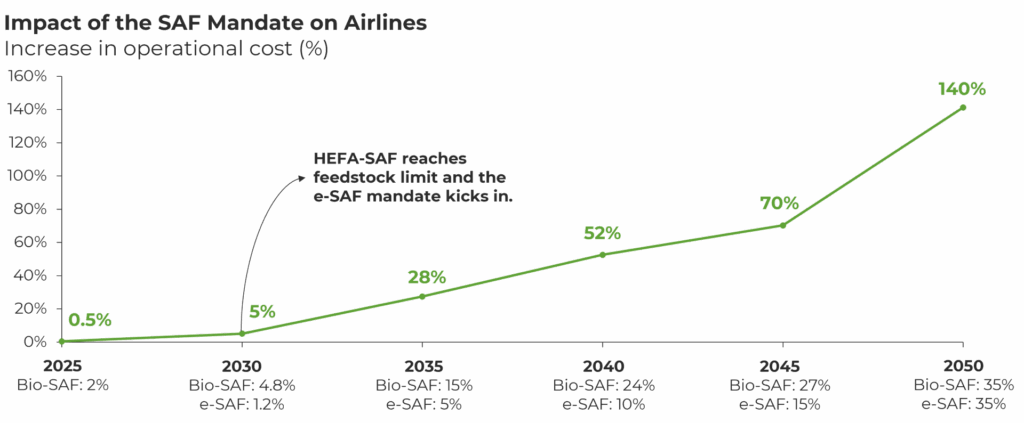

Lux Research did a high-level analysis looking at the impact of SAF adoption on airline costs. We used data from the U.S. Federal Aviation Agency to estimate the proportion of fuel costs related to total opex for a wide-body airplane and then assessed the impact of SAF adoption on these costs (note: actual operating costs will vary by airline, route flown, geography, and type of airplane; this analysis is meant to be indicative at best).

The analysis shows the impact of the EU’s SAF mandate on the cost of flying an airplane. We assumed a scenario where:

- HEFA-SAF meets the entire bio-SAF demand from 2025 to 2030.

- After 2030, HEFA-SAF production peaks as we run out of waste oil feedstock. To meet remaining bio-SAF demand, producers shift to FT-SAF using biomass feedstocks.

- We assume that ATJ-e-SAF meets all e-SAF demand, since the methanol-to-jet pathway is more cost-effective than FT.

As can be seen from the results, the SAF mandate will wreak havoc on the EU’s aviation industry. In 2025, the 2% SAF mandate will increase operational costs by only 0.5%, which can be considered acceptable for an airline. However, things change dramatically starting in 2030. The lack of HEFA-SAF means that the industry will have to rely on the more expensive FT-SAF to meet its bio-SAF demand. As for e-SAF, it is so expensive that even low adoption leads to very high increases in cost. Airlines have low margins: A 28% increase in costs is not feasible.

But that’s not all. Suppose the EU enforces the SAF mandate fully: Will Europeans stop flying due to higher ticket prices? Not entirely, because the mandate creates an unintended consequence. It applies to all flights departing from or arriving in the EU, regardless of the airline’s origin. Consider this example: A traveler flying from Paris to Singapore can choose a direct flight with Air France or a connecting flight with Emirates via Dubai. Both airlines must comply with the SAF mandate on departure from Paris. However, once Emirates lands in Dubai, it’s no longer subject to EU rules since the UAE has no SAF mandate. As a result, Air France must use SAF for the entire Paris-Singapore route, while Emirates only uses it from Paris to Dubai and completes the Dubai-Singapore leg with cheaper fossil fuel.

The fact that EU cannot impose its mandate on other countries is a major pitfall of this legislation. European airlines already face tough competition from the likes of Emirates, Etihad, and Qatar Airways, and the SAF mandate will essentially force them to cease their Asian routes. This is not a far-fetched idea: European airlines such as Lufthansa and British Airways have already cut down their flights to China as they are unable to compete with Chinese airlines that have unrestricted access to Russian airspace and can thus offer cheaper fares. The SAF mandate will have the same effect but at a much larger scale.

Outlook

I am not advocating for the elimination of the SAF mandate. SAF remains the best technology for decarbonizing aviation and a mandate is the best tool to drive adoption. However, the EU’s SAF mandate is reminiscent of its hydrogen ambitions: lofty but ultimately unrealistic. The most egregious feature is the 35% e-SAF sub-mandate by 2050. Even during the drafting of the SAF mandate, it was clear that e-SAF would remain highly expensive. Yet the EU pressed ahead with an enormous 35% target. By contrast, the U.K. adopted a far more realistic e-SAF sub-mandate of just 4% by 2050.

A mandate compels adoption, but it does little to reduce the cost of SAF technologies. The only way for the EU to achieve its targets in the current SAF mandate is through technology innovation. Companies such as Air Company and OXCCU have recently unveiled novel technologies that promise to significantly reduce the cost of e-SAF, but they are currently at an early stage of development. I have been tracking start-ups in the fuel space for almost a decade, and in my experience, 6 – 10 years is just enough to fully validate, scale, and build one commercial facility based on a novel fuel technology. Unfortunately, the EU will need a lot more than just one facility to meet its 2035 target.

Ultimately, the EU will have to revise its SAF mandate. It needs to be ambitious but also achievable – for that to happen, the e-SAF sub-mandate needs to go or at the very least, be tempered down. Forcing aviation to adopt the most expensive fuel to meet half of its mandate by 2050 is reckless. Instead of preselecting technological winners and putting a ceiling on bio-SAF, the EU should structure its mandate to prioritize SAF with the lowest carbon intensity, regardless of production pathway.