Green hydrogen has emerged as a critical pillar of global decarbonization strategies. As the urgency to reduce carbon emissions grows, hydrogen is no longer just a theoretical solution; it’s an essential piece of the clean energy puzzle. Yet for all its potential, green hydrogen remains expensive, and the technologies to produce it at scale are still maturing. The EU, one of the most ambitious regions in developing a hydrogen economy, offers a compelling lens through which to examine both the promise and pitfalls of green hydrogen.

Why hydrogen — and why now?

Hydrogen plays a dual role in the clean-energy transition. It serves as a low-emissions fuel and as a feedstock for industries like chemicals, steel, and refining. Recognizing its strategic importance, the EU has enacted bold policies to accelerate hydrogen adoption. Under the Renewable Energy Directive, EU Member States are legally bound to ensure that by 2030, at least 42% of hydrogen used in industry and 29% in transportation is renewable. The overarching target is to produce and import 20 million tonne of renewable hydrogen annually by that deadline.

However, five years from the target date, the EU is nowhere near where it needs to be. As of 2024, it had produced just 27,000 tonne of green hydrogen — less than 1% of its goal. The reason for this shortfall is as straightforward as it is problematic: Green hydrogen remains prohibitively expensive.

The cost barrier

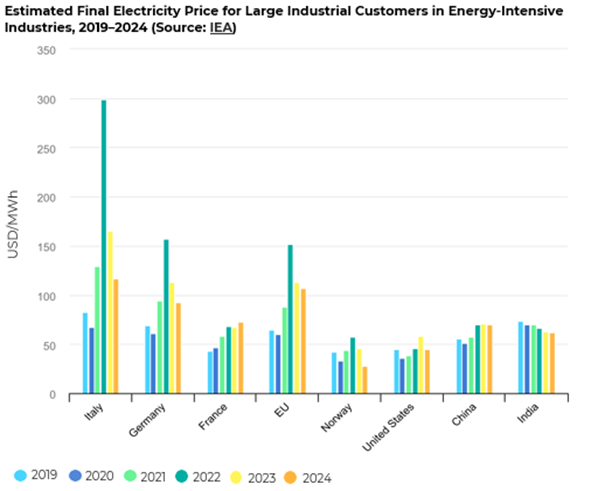

At the heart of the EU’s hydrogen dilemma lies the issue of production costs. In the Netherlands, for example, the levelized cost of hydrogen hovers around EUR 14/kg. This figure, driven primarily by high electricity prices and capital expenditures, makes green hydrogen uncompetitive compared with fossil-based alternatives. And while some countries like Spain show marginally better economics, the cost challenges are widespread across the EU.

These unfavorable economics have led to the cancellation of multiple large-scale hydrogen projects. Even outside Europe, similar projects have been put on hold, jeopardizing the EU’s ability to meet both its domestic production and import targets. With neither path proving reliable, the region risks falling short of its climate ambitions unless new, cost-effective technologies are rapidly deployed.

The rise of hydrogen 2.0

To bridge the gap between ambition and reality, the industry is turning toward next-generation electrolysis technologies that promise to dramatically reduce the cost of green hydrogen. These innovations, categorized by Lux Research as Gen 1, Gen 2, and Gen 3 technologies, offer a clear trajectory toward lower electricity consumption and, consequently, lower production costs.

Gen 1: Hydrogen at EUR 5.11/kg

The first generation, often described as traditional electrolysis, relies entirely on electricity to split water into hydrogen and oxygen. One example is Thyssenkrupp’s zero-gap alkaline electrolyzer, which achieves greater than 82% efficiency by minimizing the space between electrodes and membranes. With optimized conditions, this approach can produce hydrogen at a cost of around EUR 5.11/kg. While still expensive, it’s a meaningful improvement over existing large-scale projects.

Gen 2: Hydrogen at EUR 4.84/kg

The second generation introduces hybrid systems that incorporate electricity alongside other energy inputs like heat, microbes, or biomass. H2Pro, for instance, uses a decoupled electrolysis process called E-TAC, which separates the hydrogen and oxygen production steps to increase efficiency and reduce the need for precious metals. Meanwhile, Ki Hydrogen leverages biomass in a nonmicrobial process that claims to produce hydrogen for just USD 2/kg. These systems reduce electricity consumption to about 44 kW/kg and bring costs down slightly further to around EUR 4.84.

Gen 3: Hydrogen at EUR 2.66/kg

The third and most transformative generation aims to eliminate electricity from the equation altogether by harnessing alternative energy sources like solar radiation and industrial waste heat. One notable example is Utility, a company piloting a solid oxide system that uses industrial offgases and steam at high temperatures to produce hydrogen. Another is SunHydrogen, which employs photoelectrochemical panels to convert sunlight directly into hydrogen. While still in early stages, these approaches have demonstrated the potential to slash electricity usage by 79% compared with traditional methods, lowering production costs to EUR 2.66/kg.

From innovation to adoption

Despite the promise of Gen 2 and Gen 3 technologies, corporate activity remains disproportionately focused on older, less efficient systems. Lux Research warns that if industrial stakeholders fail to engage with these emerging technologies, the window for achieving meaningful cost reductions may close. Startups, which are driving most of the development in next-generation hydrogen production,will need partnerships with established players in energy, manufacturing, and finance to succeed at scale.

Looking ahead

The next five years are critical for the hydrogen economy. If the EU and other global leaders are serious about their net-zero goals, they must invest in and accelerate the deployment of next-generation hydrogen technologies. This means moving beyond traditional electrolysis and embracing hybrid and thermochemical methods that promise both economic and environmental gains.

For industrial players, the message is clear: Pilot advanced hydrogen systems now or risk being left behind. For policymakers, subsidies and support mechanisms must be extended to emerging technologies, not just conventional systems. And for investors, the evolving hydrogen tech landscape presents both a challenge and an opportunity — those who back the right innovations stand to benefit from a rapidly expanding market.

To learn more about how Hydrogen 2.0 is the key to unlocking a more resilient energy future, watch our webinar “The Next Wave of Hydrogen Tech.”