The Lux Take

Over the next five years, clients can expect livestock health monitoring to remain a relatively small investment space, with annual funding likely to stay in the USD 200 million–USD 300 million range. However, momentum is expected to shift from stand-alone data analytics platforms toward integrated hardware systems that use machine learning (ML) to generate actionable insights, particularly in areas like wearable devices, environmental monitoring, and computer vision.

Challenges in livestock production and the role of monitoring technologies

Livestock production faces numerous challenges, including managing animal welfare, reproductive cycles, disease prevention, and input efficiency. Feed costs can account for up to 70% of total livestock expenses, so optimizing nutritional inputs and verifying weight gain and product quality are essential. Livestock health monitoring technologies support producers and a broad range of stakeholders across the value chain, including feed additive developers, livestock pharmaceutical companies, genetics companies, and vertically integrated livestock operations. Venture capital (VC) funding for livestock health monitoring has reached nearly USD 1 billion over the past five years.

Funding trends in livestock health monitoring technology

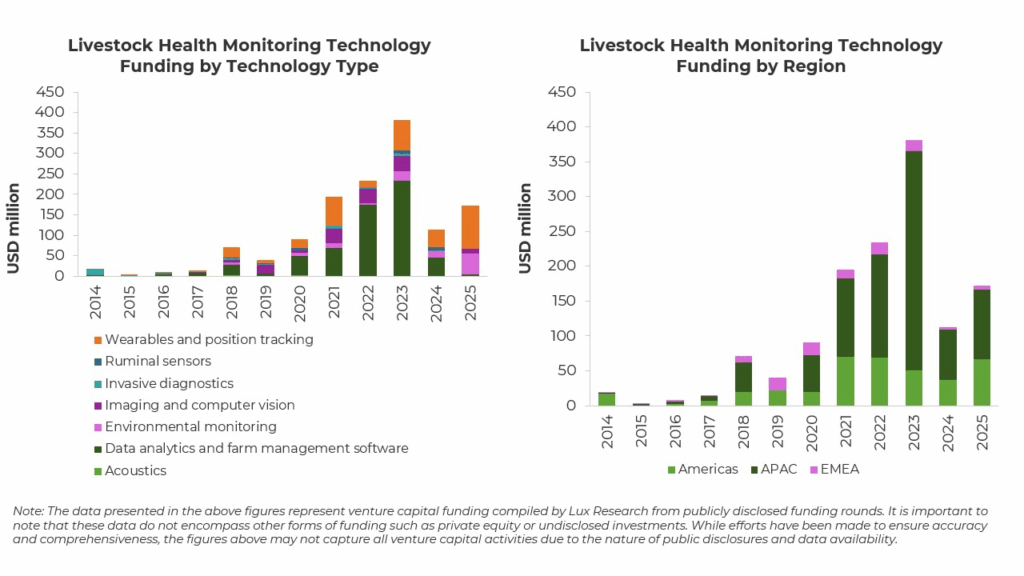

Compared with precision agriculture, livestock health monitoring has attracted less VC even with several startup developers in the space. The median funding round is USD 1.3 million. Despite smaller round sizes, funding has remained relatively steady since 2021, with the exception of a peak in 2023. In this brief, we analyze livestock health monitoring technology investments across seven categories: wearables and position tracking, ruminal sensors, invasive diagnostics, imaging and computer vision, environmental monitoring, data analytics and farm management, and acoustics.

Regional trends

In this section, we analyze the investment trends for each world region individually and discuss how these trends may impact future innovation opportunities in this space.

1. APAC leads global funding with two of the largest rounds

Despite hosting fewer developers, APAC leads in VC funding with USD 798 million raised over the past five years, accounting for 67% of total financing in this technology sector. Indonesia, New Zealand, India, and China receive the most funding in the region. Despite having fewer developers, APAC has hosted two of the largest funding rounds in the livestock health monitoring landscape.

2. The Americas show steady activity but remain underrepresented

The Americas follow APAC in VC funding, capturing USD 313 million over the past five years, accounting for 26% of the total funding. The U.S., Canada, and Brazil host the most well-funded developers in the region. Aside from BinSentry’s USD 80 million raise, the underrepresentation of the Americas in the funding landscape is likely due to small funding rounds, undisclosed funding, and acquisitions and the presence of enterprise-scale developers. However, the gap in funding in the mature large-scale livestock sector indicates a lack of alignment.

3. EMEA lags in funding despite strong developer presence

EMEA, similarly, despite representing the second-largest number of developers, lags in funding, capturing USD 74 million or 6% of funding in the past five years. The Netherlands, the U.K., and Norway have attracted the most funding in EMEA. EMEA developers have primarily focused on dairy applications.

Investment trends

In this section, we analyze the investment trends for each of the categories individually and discuss how these trends may impact future innovation opportunities in this space.

1. Wearables and position tracking become the most funded category

Wearables and position tracking has, in the past three years, moved from an underfunded small technology category to the most well-funded category of livestock health monitoring in 2025. Position tracking and wearable technology have primarily been targeted for pasture-based livestock, allowing for virtual fencing and movement of livestock without fencing, reducing labor costs and time; biometric data includes key reproductive monitoring like estrus and heat detection. Wearable and position tracking have become, over the past three years, the most funded category of livestock health monitoring technology. Despite accounting for a smaller amount of developers in the space; developers like Halter and NoFence, virtual fencing developers that support collar-based movement of cattle on pasture, have secured some of the most significant funding in livestock health monitoring in the past five years, with NoFence securing USD 35 million in October 2025. Halter secured USD 100 million in Series D funding in June 2025.

2. Ruminal sensors remain the least funded category

Ruminal sensors are the least-funded category, unlikely to gain momentum to commercialization at scale. These sensors are in-rumen biometric devices that provide information on in-rumen temperature, pH, and material movement to track microbial health, digestion, and feeding behavior. They are used most b

Invasive diagnostics, despite fewer developers, have well-funded developers focused on solutions for dairy. The technology supports livestock producers’ ability to identify key diseases using blood and other biological samples, allowing producers to detect individuals impacted by disease and obtain more rapid diagnostic results. This category has fewer developers and has overall attracted less funding. Mastitis has been one of the most targeted diseases, as it lowers productivity, compromises milk quality, and spreads easily on shared milking equipment. Advanced Animal Diagnostcs is the most well-funded developer in the space, raising USD 50 million, focusing on early detection of mastitis in dairy and bovine respiratory risk in beef. Developers Biotangents, which has raised USD 10 million, and Mastaplex, which has raised USD 8.5 million, both focus on diseases impacting the dairy industry.

3. Imaging and computer vision funding driven by aquaculture and in ovo sexing

Despite ongoing R&D in disease detection, the most funded imaging and computer vision applications are in aquaculture, in ovo sexing, and meat processing. Imaging and computer vision uses cameras with on-board or cloud computing and ML to support the monitoring of livestock remotely and allow for early categorization and alert producers to changes in livestock behavior, monitor the animal’s growth, body score, development, and feed and water intake, and track and differentiate individuals. Despite several developers’ applying solutions for disease detection and feed efficiency, developers creating sexing technology for hatcheries and supplying broiler and laying chicks have secured some of the largest funding rounds, including InOvo, which has raised USD 81 million, and Targan, which raised USD 51 million. In some cases, imaging and computer vision technology has been incorporated into enterprise-scale livestock. For example, in 2022, Cargill partnered with developer Knex to create Birdoo, a 3D imaging tool that allows for an estimation of broiler weight with 95% accuracy.

4. Environmental monitoring remains slow to commercialize

While the link between environmental quality and livestock productivity and risk is well established, environmental monitoring remains a lagging technology area, and few developers are likely to break through to full commercialization. Environmental monitoring platforms track ambient air and environmental quality, including temperature, humidity, ventilation, ammonia levels, and greenhouse gas levels in swine barns, poultry barns, dairy parlors, and feedlots. These environmental factors can impact animal welfare, productivity, and disease risk despite being most developed by enterprise-scale developers like DeLaval. MOVA Technologies, which monitors ammonia in poultry houses and develops a filtration system to reduce ambient ammonia levels, secured USD 2 million in 2025. BinSentry, which, unlike other developers, monitors grain bin environmental conditions in addition to grain and feed use, has secured USD 50 million in 2025, one of the largest funding rounds of the year. Cargill partnered with BinSentry in February 2025 to become an exclusive distributor of its AI-powered sensor in Brazil, building on the companies’ existing relationship.

5. Data analytics platforms maintain the largest share but momentum has slowed

Momentum in data analytics platforms has slowed, but it is still the most well-funded category. Developers building connectivity across livestock supply chains continue to receive funding, with data analytics and farm management platforms offering producers integrated views of on-farm metrics like animal behavior, health alerts, feed efficiency, reproductive events, and weight and body scoring. Although this remains the largest developer category across all livestock species, funding has slowed over the past five years after peaking in 2023 when eFishery, an end-to-end platform connecting shrimp and fish farmers from feed purchasing to market access, raised USD 200 million and reached USD 370 million in total funding. Venture investment has since cooled as corporate-scale players acquired many of these platforms, yet select developers continue to raise capital: AgriWebb, focused on downstream supply-chain connectivity, secured USD 7.3 million in 2024, while Antler Bio, specializing in herd genetics analytics, raised USD 4.3 million in 2025.

Acoustics remains an underfunded and underdeveloped space, despite potential to capture and provide analytics similar to computer vision and imagery at a lower cost. Acoustics uses sound to track livestock health and welfare, including early warnings of piglet crushing and early detection of disease, such as coughing in swine and poultry. Acoustics has been the least funded technology space. BioFeeder has secured USD 4.3 million in funding to use acoustic signals in shrimp aquaculture production to adjust feeding. SoundTalks is one of the most advanced developers, with a commercially available product and a partner, Boehringer Ingelheim, which holds a minority stake in the company.

Outlook

As in precision agriculture, data analytics and management platforms make up the largest share of livestock monitoring developers and funding, though momentum has slowed due to consolidation and competition. Developers focused on downstream market connections continue to attract investment, while wearables and position tracking, computer vision, and environmental monitoring are still growing, with wearables and tracking becoming the most funded category in 2025. Aquaculture-focused developers lead overall, with developers like Indonesia-based eFisheries capturing some of the largest funding rounds, accounting for 28% of livestock health monitoring funding over the past decade, followed by beef and dairy solutions at 25%, dairy-only tools at 17%, and poultry and swine at 9%. The species funding reflects both sector needs and production needs. With focuses on market connection being core challenges for disaggregated sectors of aquaculture, beef, and dairy and for dairy production systems, long-lived and highly managed animals require greater investment per animal. Clients can expect continued investment in technologies that improve feed and labor efficiency, strengthen downstream market connections, and integrate data across supply chains.

To learn more about these investment areas, connect with a Lux analyst.